本文共字,预计阅读时间。

一直以来,女性在金融服务行业中都处于相对弱势的位置。以我国为例,2016年的统计数据显示,超过50%的大陆女性无法获得基本的金融服务。对此,万事达卡国际市场总裁Ann Cairns认为,金融服务的不平等也是性别不平等的表现,女性应该是发展普惠金融的重点人群,金融机构应该为她们提供必要的工具和技术来充分挖掘自身潜能。随着人类文明进入电子科技时代,不同于工业时代对严谨以及力量的高要求,如今的世界更重视精细和感性的价值,那么,女性特有的感性、空间感和想象力能否在这个时代展现出别样的魅力和风采呢?Scott Saunders和他的产品Joy开启了一场别样的探索。

不走寻常路 Joy以用户体验取胜

此前,金融领域也出现了许多针对女性群体的金融服务平台,但它们大多选择了一种"学院派"的风格,试图通过推出简单、高效、严谨的个性化金融辅导程序提高女性的金融活动参与度。然而,这些常识大多事与愿违,并未取得良好的效果。

与以往不同,作为在线借贷平台Payoff的首席执行官,Scott Saunders则另辟蹊径,从用户体验入手,吸引更多女性参与到金融活动中来。

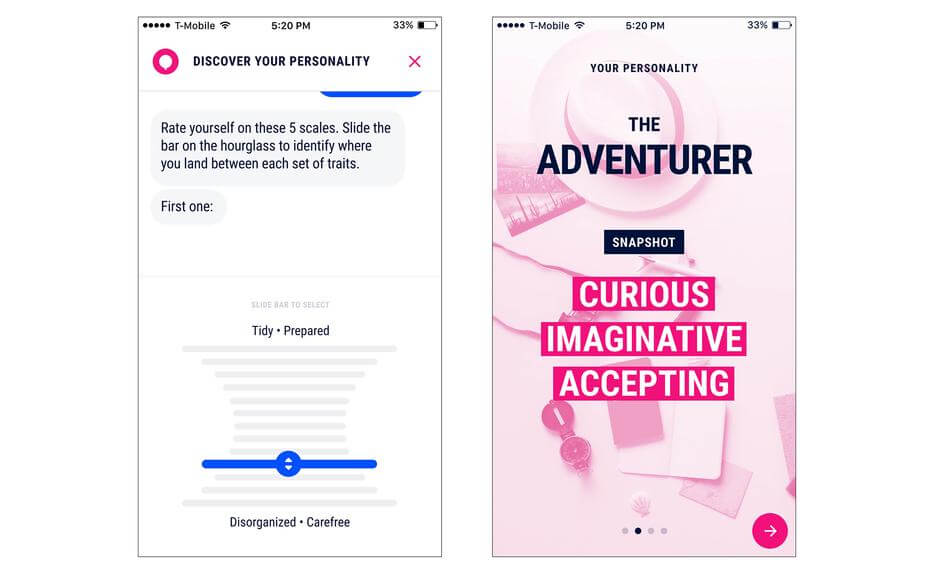

早在2014年,Scott Saunders就组建了一支包括心理学家、认知精神学家、市场营销人员以及eHarmony匹配算法程序员(eHarmony是美国最大的婚恋交友网站之一,通过心理和性格测试为男女进行婚恋匹配)的产品研发团队,并开始研发一款以心理测试功能为基础的金融服务程序。在登陆该程序后,用户需要首先接受一套心理和性格方面的评估,之后,系统将根据评估结果为用户匹配智能化的金融服务流程。Scott Saunders试图通过将金融与心理学进行结合,减轻用户在参与金融活动中所产生的压力,提高趣味性。

历时将近三年,这款名为Joy的程序终于在本月初正式上线,用户可以免费登陆获取服务。该程序在研发过程中采用了近年来火爆的人工智能技术,使得操作流程更简洁易懂,也更具针对性。

据Joy的研发团队透露,该产品的初步发行结果显示,女性用户数量远远高于男性。鉴于此结果,他们又与时尚设计公司Alison Brod进行合作,对Joy的外观进行了进一步的改善,包括采用了更加明亮的配色方案以及增加了气球图案。对此,Scott Saunders表示,公司将加大对男性用户的宣传力度,但他也强调,Joy的目标用户群体一直是女性,希望该产品的趣味性能够吸引更多的女性用户参与到金融活动中来。

随着经济和社会的进步,尽管女性的收入一直呈现增长的态势,且对自身财务的控制能力也在不断增强,但是出于种种因素,女性在金融服务活动中的参与度还远远低于男性。Scott Saunders举例称,埃森哲发布的一份2016年金融活动参与度报告显示,超过58%的男性在过去一年中有过"财务咨询"的经历,而女性只有44%。此外,有75%的男性表示了解基本的投资活动,而女性只有61%。

美国富达投资集团高级副总裁Alexandra Taussig认为,当今世界金融体系中的一切资源和标准都是以男性为导向的,而Joy的出现则极有可能打破这一局面,为女性在金融世界中谋求更加关键的地位。埃森哲全球财富管理总经理Kendra Thompson也表示了赞同,他认为,现代女性更为关注某一活动的远期效益,在面对风险时,甚至比男性更为果敢,然而,当前的大部分行业并没有真正关注到这一点。

LearnVest和Ellevest的探索

LearnVest是一家2009年成立于美国的专为个人提供理财计划咨询与理财教育的网站。公司的创始者Alexa von Tobel学生时期就读于哈佛大学,并在2008年申请从哈佛退学开始创业。据von Tobel称,由于自己与公司许多高层管理者为女性,因此她们在确定服务目标时调查了女性理财市场,发现家庭中大部分的财务大权由女性掌管,但这些女性并没有专业的理财知识;另外,为了避开与当时行业中已有的理财平台进行正面竞争,LearnVest当时决定做细分市场,只为女性特别是家庭主妇提供理财服务。刚成立的LearnVest由于针对女性市场这一特点获得一轮轮的投资,迅速发展业务,既避开与老牌机构的正面冲突又成功吸引用户与投资机构的注意。

平台从最开始提供免费的个人理财攻略到后来的收费理财咨询再到理财教程,从最开始只针对女性用户到自2011年始也对男性用户开放,一步步完成了业务的完整与客户定位的改变。2015年,美国人寿保险和资产管理公司Northwestern Mutual宣布以2.5亿美元的价格对LearnVest进行收购,届时,该平台已拥有200万名免费用户和1万名付费用户。

2014年,前美国银行行长,花旗集团首席财务官Sallie Krawcheck创办了Ellevest,这是一个女性专属的智能投资顾问服务平台,以满足女性投资者的需求为宗旨,承诺将女性的预期薪资、职业生涯转折纳入考量范围,还会很贴心地将女性群体的特征和需求作为提供专业建议的前提考虑。

Sallie Krawcheck表示,Ellevest在未来将会不断升级,完善服务体系,不仅要为女性群体打开一个新窗口,更远的目标则是颠覆传统投资界男性垄断的现象和概念。截止到今年年初,Ellevest已经获得了超过1900万美元融资。

对于LearnVest和Ellevest在提高女性金融地位方面的贡献,另一家针对女性的金融服务平台WorthFM的创始人Amanda Steinberg给予了肯定,她认为,其实女性并非想在金融领域中获得特殊优待,她们只是在争取外界对于她们能力的肯定。

Joy的发展前景

Joy的核心竞争力在于,通过对用户心理评估和其他财务数据的分析,为用户指定个性化的理财方案。系统将从5个方面对首次登陆的用户进行评估,并根据评估结果,将用户与系统中的10个智能投顾进行匹配,提供理财服务。同时,Joy系统还能够通过分析用户的收入、支出、信用情况、服务满意度等数据,随时为用户调整理财策略,使服务更加个性化。在服务结束后,系统还将对结果进行跟踪,并评估整个服务流程,完善自身性能。

尽管如此,部分业内专家还是明确表示,用心理测试来作为金融活动指导的依据简直是无稽之谈。美国圣塔克拉拉大学的金融学教授Meir Statman认为,Joy所推行的心理评估内容与实际的金融活动之间的联系程度极低,很难作为指导依据。此外,随着时间的推移,系统的人工智能程序也需要不断完善以适应用户的行为变化,虽然Joy系统的服务跟踪程序有可能会弥补缺陷,但该程序能否真正达到预期的效果还有待观察。

非常感谢您的报名,请您扫描下方二维码进入沙龙分享群。

非常感谢您的报名,请您点击下方链接保存课件。

点击下载金融科技大讲堂课件本文系未央网专栏作者发表,属作者个人观点,不代表网站观点,未经许可严禁转载,违者必究!

本文为作者授权未央网发表,属作者个人观点,不代表网站观点,未经许可严禁转载,违者必究!

本文版权归原作者所有,如有侵权,请联系删除。

京公网安备 11010802035947号

京公网安备 11010802035947号