本文共字,预计阅读时间。

编者按:尽管美国在技术创新的很多方面都是领先中国,但起码有一个领域是中国领先的。这个领域就是以在线支付和移动支付为代表的金融创新。这一切究竟是如何发生的呢?彼得森国际经济研究所(PIIE)总结了两大原因:1)信用卡的欠缺以及互联网公司的发展刺激了在线支付系统的需求;2)法律保障、监管宽松以及智能手机为在线支付系统的发展提供了动力。

去年中国的一项调查发现,84%的中国人并不担心出门不带钱——这不是因为他们对信用卡或者支票形成了依赖,而是因为他们对自身移动手机的支付手段,比如支付宝或者微信能够被接受很有信心——不管金额多少。中国似乎,至少在这个领域似乎已经超越了美国,因为美国人还在执着于塑料卡片(信用卡、借记卡),以及支票和现金这些东西。中国俨然已经站上了未来金融技术潮头浪尖。这是怎么发生的呢?

关于中国最近金融科技的发展及其对全球商业的影响我们撰写了三部分组成的系列文章,本篇有关中国在线支付崛起的文章是第一篇。

信用卡的欠缺以及互联网公司的发展刺激了在线支付系统的需求

值得注意的是,中国快速发展的第一个要素是中国2000年代早期时支付基础设施的落后,与此同时,互联网公司正好开始扩张。电子商务公司被迫开发自己的支付工具,从而建设成业务遍布全国范围的企业,这是他们的美国同行做不到的。当美国的互联网公司在1990年代开始腾飞时,信用卡已经无所不在并且加入了国际网络。美国的电子商务网站只需要接受信用卡就能处理来自全国任何地方甚至海外的支付,并且具备发起退款的能力(如果订购的商品一直没到货的话可以轻易取消支付),这让买家感到更加安心。退款是信用卡的一项经常被忽视的比较优势(相对于借记卡和银行转账)。

而在2000年代早期的中国,大家基本上还没有听说过信用卡,网上银行也很罕见,借记卡也不能在全国范围使用。实际上,让中国对美国的信用卡开放成为了美国的一项主要的政策目标,这个进程已经被拖了10年,只是最近才得到开放——美国运通设立了一家合资企业。中国体系的原始属性可以在当时在线点对点拍卖网站易趣网的支付过程得到体现:于1999年成立的这家在线公司必须解决一个大麻烦——为其客户所在的每一座城市的每一家主要银行设立独立的账号,因为借记卡只能在同一座城市的同一家发卡银行使用。为了避免跟这套臃肿笨拙的系统打交道,易趣网只好靠送货的接受货到付款。类似Visa和万事达的中国银联到2002年才推出,然后才慢慢地将不同城市和银行之间原先碎片化的系统整合起来。

与此同时,腾讯(中国最大的社交与游戏公司)和阿里巴巴(中国最大的电子商务公司)都建立了自己的支付系统来解决自身业务的特定问题。2002年,腾讯创建了一种虚拟货币——Q币,其客户可以用这种货币来为聊天形象购买游戏物品、数字装备之类的数字产品。其功能类似于礼品卡,这样一来客户跟银行体系完成一次大型的Q币购买之后就能方便地在腾讯系统内用Q币进行网上交易了。

阿里巴巴这种2004年的时候推出了支付宝(现为蚂蚁金服的一部分)用于淘宝的交易。一开始支付宝是作为相互不信任的购买参与者的第三方支付服务的身份出现的。易趣网早在2002年的时候也尝试过第三方支付服务,但这项服务费用太高,所以做不起来。支付宝一开始的免费服务是想将支付推迟到商品到达,这样买家就能在东西一直没到或者是假冒伪劣时信任阿里巴巴可以把钱退给他们了。美国的信用卡退款几乎是一样的功能,所以美国公司就没有太大必要自己去建支付系统来解决这个信任问题了。信用卡的接受度使得第三方支付对eBay和Amazon来说没那么重要。

法律保障、监管宽松以及智能手机为在线支付系统的发展提供了动力

在线支付系统发展的第二个关键因素是中国政府的支持。中国2004年的电子签名法为在线合同提供了法律确定性,2005年开始《国务院办公厅关于加快电子商务发展的若干意见》等一系列政策表态也为在线支付提供了宽松的政策条件。易趣网的第三方支付之所以失败,部分原因也许是因为它出来得太早了,签名法律还没有到位,而支付宝正好是在法律风险没那么大的时候推出。中国央行等待了好几年,直到2010年才开始通过对该板块的官方监管,并在此后很快发行牌照,这使得市场可以在几乎没有合规性成本、准入门槛以及监管限制的情况下自由发展。相反,美国像Paypal这样的公司却要经历一个逐州进行的、低效的、碎片化的流程来获得货币转移商牌照。

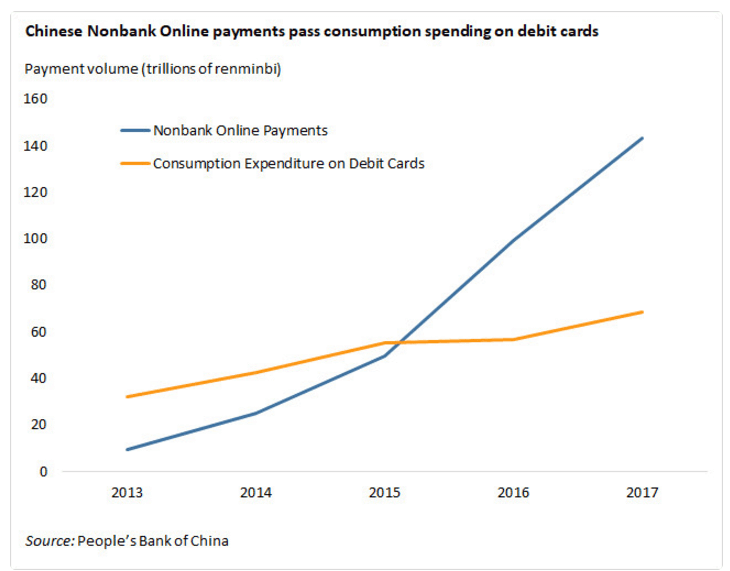

因此,等到监管介入时,像支付宝这样的非银行支付系统已经有将近10年的历史;而到那个时候,由于网络效应以及数亿中国人都用上了智能手机,它们已经达到了临界规模,从而推动在线支付朝着移动支付转移。2013年非银在线支付一下子成为了全球的焦点,当年中国的非银支付处理的交易量达到了9.2万亿元(参见下图)。同样在2013年,支付宝超越了PayPal成为全球最大的在线支付平台。在2013年(第一年提供在线支付量的官方数据)之前对其增长的量化是非常困难的,因为阿里巴巴和腾讯对自己的数据是保密的。2014年非银在线支付几乎增长了170%,并且很快就超过了中国50万亿元左右规模的借记卡消费开支。

黄色:借记卡消费支出;蓝色:非银在线支付

黄色:借记卡消费支出;蓝色:非银在线支付

中国互联网公司的金融科技创新取得了成功

中国在线支付的成功收购互联网公司共生关系的结果,这为他们的支付业务提供了原生的用例。鉴于电子商务占到了中国零售销售的17%,而美国的相应数字是8.9%,所以相对于美国,在线支付更适合于中国的环境。包括小商贩在内的线下业务的采用,比如采用二维码代替NFC或者塑料卡来进行个人支付对此也起到了帮助作用。线下商家使用买家智能手机摄像头来扫描印刷的二维码(或者类似条形码这样的扫描枪来扫描买家智能手机屏幕上的二维码)。这种办法比设立昂贵的联网销售点设备要容易得多,尽管像Square这样的公司已经让美国做这样的事情变得便宜多容易多了。

在在线支付已经根深蒂固之后,腾讯和阿里巴巴的蚂蚁金服还把业务扩展到借贷及资产管理这样的领域。中国的一个关键经验是这些变化不是一夜之间发生的。开发这样的基础设施需要好几年的时间,需要有足够多的消费者信任互联网公司接管其金融生活。但也许最重要的是,金融科技创新之所以出现是因为少数公司无法忍受其环境中有缺失的环节。他们宁愿开发新的、更高效的系统而不愿等待既有者替他们这这件事情给做了。

非常感谢您的报名,请您扫描下方二维码进入沙龙分享群。

非常感谢您的报名,请您点击下方链接保存课件。

点击下载金融科技大讲堂课件本文系未央网专栏作者发表,属作者个人观点,不代表网站观点,未经许可严禁转载,违者必究!

本文为作者授权未央网发表,属作者个人观点,不代表网站观点,未经许可严禁转载,违者必究!

本文版权归原作者所有,如有侵权,请联系删除。

京公网安备 11010802035947号

京公网安备 11010802035947号