本文共字,预计阅读时间。

当全球的风险投资者把目光聚集在英国、美国、中国等Fintech强国时,地处于欧亚十字路口的土耳其也在不声不响地布局着自己的金融科技版图。

近年来,尽管受到国内政治因素的影响,但土耳其的金融科技行业还是表现出了强劲的发展势头,逐步构建起了独具特色的金融科技"生态系统"。国内最大城市伊斯坦布尔更是汇聚了大量金融科技领域的尖端人才,再加上其独特的地理位置,多次被业内专家提名,计划将建设成为连接欧亚市场的金融科技中心。

现阶段,土耳其计划将加大对全球其他金融科技中心的关注度,尝试从中探索出符合国情的金融科技之路。

放眼全球的金融科技强国,以色列与土耳其具有相似的地缘政治环境。在过去十年里,以色列在金融科技行业取得了令人瞩目的成就,其国内第二大城市特拉维夫已经成功跻身世界前五大金融科技中心。

目前,在以色列获得的全部投资中,有75%来自国外投资者。截止到2016年,以色列总人口达800万。相比于其他国际金融科技中心,显然其国内市场需求有限,但这并不能阻碍巴克莱、花旗、维萨、Paypal、万事达卡、桑坦德银行等众多金融巨头投入大量资金,在以色列兴建金融科技研发中心和加速器。

以色列金融科技产业的成功代表着自身国情与全球大环境的完美结合,但发展过程中所展现的一般规律仍值得其他国家深度借鉴。

创业准备时间

在任何行业中,创业者在创办公司之前,都需要向政府申办营业许可证等一系列证件。因此,该流程的持续时间,即政府的工作效率,对企业的前期发展具有重要的影响。

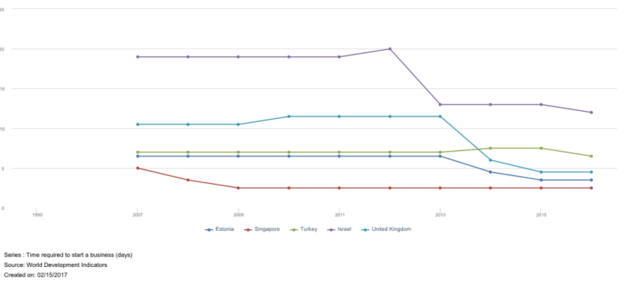

据世界银行统计,以色列的创业公司平均需要12天时间进行前期准备。截止到2016年,对于经济合作组织的成员国,该数字为8.13天,而土耳其的创业公司只需要6.5天的准备时间,就可以开展业务。

显然,政府工作效率低下是阻碍以色列创业公司早期发展的因素之一。然而,这并不能阻碍以色列金融科技产业的发展,目前,该行业已成为推动以色列GDP增长的主要动力,超越英国和美国。

下图显示了各国创业公司开展业务所需的准备时间。

创业启动成本

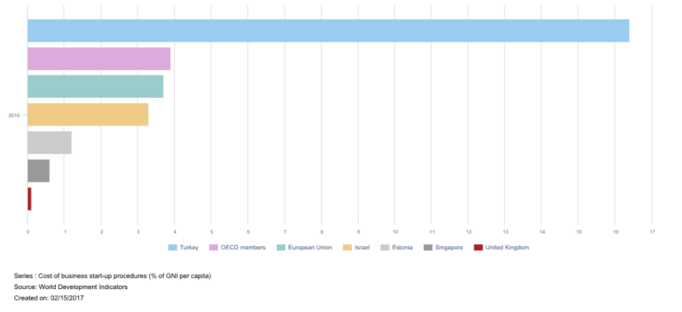

以色列金融科技创业公司的启动成本远低于欧盟平均水平,更接近于新加坡、爱沙尼亚、英国等金融科技强国。

下图显示了各国创业公司的前期启动成本。

尽管相对低廉的前期启动成本有利于以色列金融科技创业公司的前期发展,但这种帮助的影响也是有限的。然而,不可否认的是,相比于其他地区的创业公司,以色列创业公司所具有的这种"先天优势"确实使得它们能够在全球市场上占得先机。

创新与专利

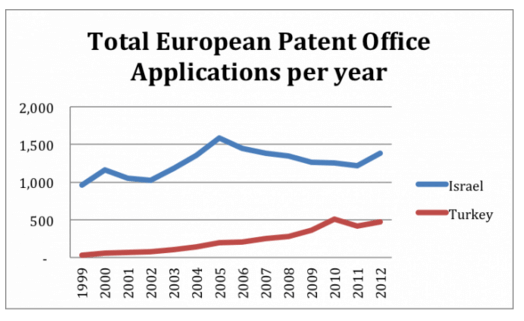

此前,欧洲专利局曾发布了由经合组织OpenData统计的土耳其和以色列的专利申请数据。

由图所示,在过去15年中,土耳其金融科技领域的专利申请数量呈现稳定增长态势,其中,2010年达到创纪录的506项。

同样,近十几年来,以色列与国外合作研发的专利数量占总专利申请数的百分比一直保持在较高的水平。但土耳其却在该方面呈现下降趋势。

政府扶植

以上所提到的统计数据其实都是在间接程度上影响一个国家金融科技产业的发展。而国家政府为扶植金融科技创业公司所提供的研发资金,则会直接加快公司的发展进程。下图展示了各国政府为扶植创业公司,所提供的资金比例。其中,以色列处于世界领先位置,仅仅落后于韩国。

在大多数国家,对企业的研发扶植资金主要由国家承担,然而,在以色列,该笔资金却由私营部门进行支付。据经合组织在2013年统计的数据,在以色列企业全年所获得的研发资金中,只要13%是由国家政府所提供的。

有关专家表示,该项数据是揭示以色列科技政策的一项关键指标。近年来,以色列政府正在逐步淡化其在资金援助方面的作用,并在积极尝试在企业发展的其他战略领域发挥领导作用。现阶段,政府主要以侧面支持的形式来促进企业的发展。通过发布政策等手段号召业内金融机构为初创公司提供支持,从而加强公司与市场的联系,有利于公司探索适合自己的发展道路。

国际合作

此前,英国政府曾与以色列达成合作,联合成立了金融科技研究中心。目前,该研究中心已汇集了数百家金融科技公司,为创业公司提供了详尽的发展规划咨询和市场前景分析,从而极大的加深了创业公司对市场的理解,促进了长远发展。

以色列政府通过进行国际合作,与外部建立伙伴关系,推进国内金融科技产品的开发,同时,加强对技术提供商和相关资讯机构的指导,以促进国内企业的高科技出口能力,从而在全球金融科技系统中保持领先地位。为了加深与国外金融科技领域的合作,以色列政府已经与美国、英国、日本和印度等多国签署了长期投资协议。

以色列政府采取的一系列制度也对中国在以色列的投资产生了巨大影响。以色列对外贸易部曾发表文件指出,1992年,中国在以色列境内的投资总额为5000万美元,而到2014年,这一数字已增长为110亿美元。

有关专家指出,目前以色列在金融科技领域所取得的成就得益于政府所颁布的一系列政策,特别是政府自2000年以来所推行的投资政策。

而土耳其的金融科技发展之路始于2012年,该年获得投资总额为110万美元。到2015年,这一数字增长了8倍。近年来,这一情况在全球的金融科技市场上屡见不鲜。世界上有大量的金融科技创业公司,尽管它们创立年份不长,但市场估值已达到数十亿美元。自2012年以来,大量的资金被注入到金融科技行业,尽管这造成了短期的市场波动,但对金融科技行业的长远发展造成了积极的影响。但也有一些业内人士指出,目前人们过于盲目关注公司的市场估值,而降低了对公司核心产品的重视。

土耳其的发展之路

土耳其金融科技行业的发展应依靠合理的制度,更不是单纯依赖投资。近年来,尽管土耳其获得了来自包括BKM在的多家金融机构的投资,但行业的长期发展还是需要国家在制度方面的支持。有关专家认为,土耳其政府应当加快在区块链、监管科技、互联网保险、在线借贷、反欺诈等领域的制度建设。

土耳其政府还应当积极寻求国际合作,向金融科技强国学习发展经验。

非常感谢您的报名,请您扫描下方二维码进入沙龙分享群。

非常感谢您的报名,请您点击下方链接保存课件。

点击下载金融科技大讲堂课件本文系未央网专栏作者发表,属作者个人观点,不代表网站观点,未经许可严禁转载,违者必究!

本文为作者授权未央网发表,属作者个人观点,不代表网站观点,未经许可严禁转载,违者必究!

本文版权归原作者所有,如有侵权,请联系删除。

京公网安备 11010802035947号

京公网安备 11010802035947号