本文共字,预计阅读时间。

在上周AltFi举办的欧洲互联网金融峰会上,英国最大的两家P2P网贷平台Funding Circle和Zopa的CEO就公司是否将在未来涉足银行业务发表了不同意见。

Funding Circle:未来绝不开展任何形式的银行业务

该公司首席执行官Samir Desai明确表示,银行的业务模式违背了公司"实现普惠金融"的发展愿景,因此Funding Circle将不会在未来开展任何形式的银行业务。他指出,随着近年来网贷行业的迅速发展,市场上越来越多的网贷机构选择与银行建立合作,拓宽自身业务范围。

目前已经出现了三种合作模式:

- 银行从网贷机构购买债权,

- 银行与网贷机构共享用户以及银行与网贷公司成立新公司,

- 打造"联合品牌"。

Desai强调,在这三种合作模式中,网贷机构只是扮演着一种"技术供应商"的角色,为银行开展业务提供良好的环境。毫无疑问,银行将成为合作中唯一的获益方,而网贷公司的作用将越来越边缘化,不利于行业的长期发展。

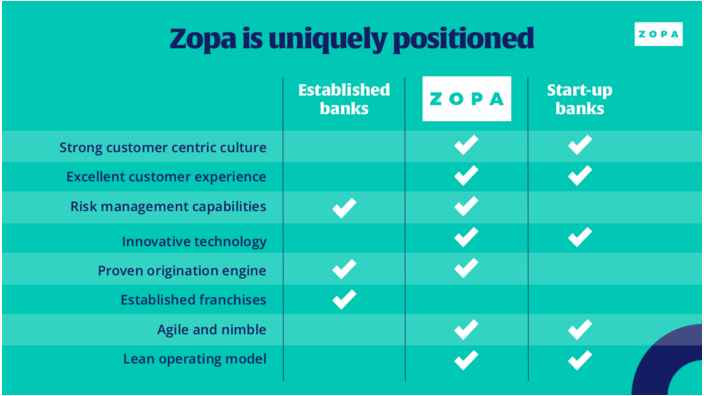

Zopa:网贷平台"银行化"将成为未来行业的发展趋势

与Desai的看法相反,Zopa CEO Janardana则认为网贷平台的"银行化"将成为未来行业的发展趋势。去年11月,Zopa曾宣布公司将于近期申请银行营业牌照,正式涉足银行业务。Janardana表示,现阶段该公司还将专注于发展网络借贷业务,特别是储蓄类金融产品的开发和销售。Zopa已经推出的储蓄类金融产品主要包括定期存款和现金ISA(在此账户中储蓄的现金所产生的利息不需纳税。这不同于普通的储蓄账户,因为普通账户要征收20%的税金)两大类。同时,Zopa还进行了平台技术上面的改进,简化了操作流程,提高用户体验。

去年1月,欧洲理事会出台了付服务法令II(PSD II),以赋予市场上的部分金融机构链接银行支付系统的权限,规范金融市场体系。Janardana认为,该法令已经导致银行用户的流失,为网贷行业拓展用户提供了极大的便利。自2011年以来,信用卡透支率逐年上涨,用户对银行的满意度也呈下降趋势,这都表明了传统银行业的发展存在诸多的问题,而Zopa所开展的银行业务则将通过自身优势有效地解决这一系列问题。

Funding Circle是英国首家专注于小企业贷款的金融机构,Zopa则是全球第一家P2P网贷平台。迄今为止,这两家公司的贷款数额均已超过20亿英镑。

非常感谢您的报名,请您扫描下方二维码进入沙龙分享群。

非常感谢您的报名,请您点击下方链接保存课件。

点击下载金融科技大讲堂课件本文系未央网专栏作者发表,属作者个人观点,不代表网站观点,未经许可严禁转载,违者必究!

本文为作者授权未央网发表,属作者个人观点,不代表网站观点,未经许可严禁转载,违者必究!

本文版权归原作者所有,如有侵权,请联系删除。

京公网安备 11010802035947号

京公网安备 11010802035947号