本文共字,预计阅读时间。

世界经济论坛2017年新领军者年会于6月27日正式在中国大连召开。政府、学校、协会等机构组织企业家代表团通过参会,充分了解全球最前沿的技术与商业模式创新,与各行业、政府领导人和国际机构的代表加强交流,分享自己的观点,提升企业形象,共同贡献社会。新领军者年会是世界经济论坛在全球范围内举行的最重要的国际性会议之一,又名"夏季达沃斯",该活动在中国已经成功举办十一届。

本次年会充分认识到了普惠金融在迈向创新、活力、联动、包容的经济发展过程中的关键作用,以及促进经济活动参与者之间有效联系的纽带地位。利用数字技术降低成本,扩大金融服务的覆盖面,深化金融服务的渗透率,将是促进普惠金融的关键。2016年,中国极大地影响并加快了数字技术的运用,以提高金融服务的可得性和包容性,从而有助于促进和推动国家层面主导的行动,这些行动在家庭、社区、国家和国际层面可产生深刻的社会和经济影响。

同时,会议指出,中国在推进普惠金融的过程中面临的最大挑战是如何真正使银行业务惠及中小企业和个人。目前,在中国的金融行业中,国有商业银行仍然处于不可撼动的地位,但银行的主要客户却是以国有企业为主。随着中小企业的迅速崛起,对金融服务的需求持续加大,使得我国的金融市场所呈现出的不平衡特点在不断加剧。

近年来,互联网技术在中国的普及,特别是移动互联技术的发展,为金融弱势群体获取金融服务提供了有效途径,同时,也在一定程度上弥补了传统金融业在新时期下的发展缺陷。在政策号召和技术进步的推动下,商业银行开始引入金融科技,积极谋求转型。

在政府和金融行业的共同努力下,中国在推动普惠金融的进程中取得了巨大成就。据波士顿咨询集团此前发布的研究报告显示,平均每个中国的成年人拥有5.36个财务账户。同时,随着中国经济数字化的趋势不断加强,以支付宝和财付通为代表的第三方支付公司开始崛起。据统计,中国的移动支付用户超过4.75亿,并且这一数字还在不断上涨,这大大加强了我国基础金融服务的渗透率。

此外,市场中还涌现出了一大批数字化资产管理公司。2013年,阿里巴巴旗下的蚂蚁金服正式推出货币投资基金余额宝,以低至0.01元人民币的投资门槛吸引了大量投资者。目前,余额宝的用户数量超过3亿,管理资产总额达到800亿元。

在网络借贷方面,除了蚂蚁金服和腾讯两大巨头外,国内目前有数千家网贷公司在分食这一市场,过度的竞争也导致了借款人的成本不断降低。截止至去年年底,中国网贷市场融资额达到1.16万亿元。

网贷市场的不断发展是对中国信用卡体系的有效补充。据统计,中国的信用卡普及率为29%,相对地,美国的信用卡普及率为34%。然而,值得注意的是,在我国网贷市场快速发展的背后,不完善的监管体制正在时刻威胁着市场的稳定发展。不过,进入2017年以来,中国人民银行、银监会等监管机构已经下发了一系列的文件,试图构建一个可预测的、以风险为导向的、公平的法律监管框架,目的在于允许有新进入者,却不过度增加非风险导向的合规成本,从而促进新兴金融行业的可持续发展。

在为个体借贷活动提供便利的同时,数字普惠金融也极大的提高了中小企业的融资效率。目前,部分金融科技企业已经推出了专门针对无银行账户的中小企业的金融服务,不仅为它们提供直接贷款,还对它们的财务情况和融资模式进行指导,协助它们获得长期稳定的融资。作为首批获得央行颁发第三方支付牌照的综合金融服务平台,LaKala致力于为中小企业提供数据分析、风险管理等服务,提高企业运作效率,扩大融资渠道。

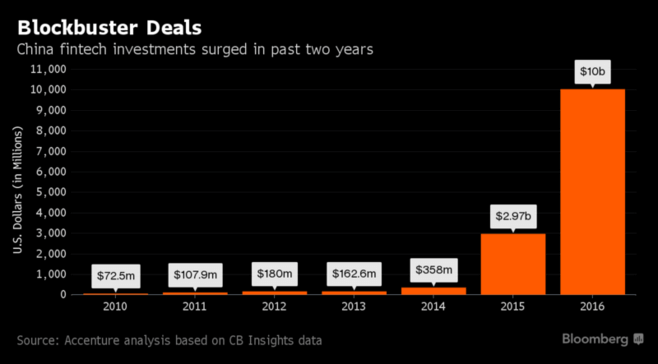

中小企业的迅速发展产生了对金融服务的巨大需求,使得中国当前世界上吸收风险投资能力最强的国家。据普华永道在去年发布的报告显示,2016年全球一半以上的金融科技领域投资投涌向中国。

然而,需要承认的是,尽管金融科技行业在中国呈现出了不可阻挡的发展态势,但在推行普惠金融的进程中,商业银行仍然发挥着主导作用。目前,我国商业银行的总资产超过200亿美元,在发展数字普惠金融方面仍具有极大的潜力。

一直以来,中国政府也积极制定政策,鼓励商业银行开展相关业务。2016年1月,国务院下发了"关于实现普惠金融的指导意见(2016-2020)",今年年初,国务院总理李克强在"两会"上再次强调了商业银行在发展数字普惠金融方面的作用,并且承诺政府将在2017年出台相关支持性政策,协助商业银行逐步上线数字金融产品。在政府的号召下,自去年4月份开始,以中国工商银行和中国银行为代表的商业银行纷纷设立了专门从事数字普惠金融的事业部。

除此之外,农村作为普惠金融的重点推进地区,也越来越多地受到了金融机构的关注。对此,中国人民银行金融保障部前部长表示,中国数字普惠金融的发展水平已经远远高于了世界平均水平。在下一阶段,政府需要做的不仅仅是鼓励金融资源更多的向农村地区倾斜,还要推行含义更为深刻的普惠金融概念,例如建立金融服务渠道、协助贫困地区企业完成上市等。

除了政策因素外,日益激烈的市场竞争也在驱动着商业银行转变发展模式。以往被传统金融行业所忽视的用户体验等因素正在被越来越多的商业银行所重视。部分商业银行选择了与金融科技公司建立合作,以弥补科技上面的劣势和扩大用户市场。2016年,中国建设银行宣布与蚂蚁金服达成战略合作,共同推进在电子支付、信用评级、在线金融服务等方面的产品研发。

随着越来越多的银行选择与金融科技公司建立合作,我国逐渐形成了参与主体更加丰富,服务范围更加广泛的多层次金融市场。在这个过程中,不断涌现出来的先进的金融科技和产品不仅将为消费者的生活提供极大的便利,也有利于提高中国在世界金融市场的竞争力。而蚂蚁金服、腾讯等互联网巨头和大型商业银行无疑将在这一过程中发挥巨大作用。

非常感谢您的报名,请您扫描下方二维码进入沙龙分享群。

非常感谢您的报名,请您点击下方链接保存课件。

点击下载金融科技大讲堂课件本文系未央网专栏作者发表,属作者个人观点,不代表网站观点,未经许可严禁转载,违者必究!

本文为作者授权未央网发表,属作者个人观点,不代表网站观点,未经许可严禁转载,违者必究!

本文版权归原作者所有,如有侵权,请联系删除。

京公网安备 11010802035947号

京公网安备 11010802035947号