本文共字,预计阅读时间。

最近几个月,几家金融科技公司相继获得许可证,可以作为银行从事经营活动——并最终成为银行。 金融科技公司的特点是规模小巧、创新性强且灵活性大。他们对传统的银行模式不仅仅是憎恶——他们甚至以瓦解这种模式为使命。 因此,这些公司选择和巨大笨重的银行同样的道路,并且真的获得许可证,似乎有违直觉。对于我们很多人来说,可能要费点脑筋,才能理解这一新的趋势。

获得银行牌照是成功商业模式的证明吗? 这些公司是否需要获得信任? 在金融科技公司的扩张大赛比赛中,这一举动是获得低成本资金来源的方式吗? 或者,这是否仅仅是一个以防其他相关因素告急(声誉,财务等)的区别性因素?

许多行业思想领袖都宣称,我们已不需要传统银行业务,因为金融科技公司能够更有效地提供相同的服务。 事实上,许多金融科技一直试图将自己定位为现有银行模式的替代品。

另一方面,许多成熟的银行试图通过收购金融科技创业公司,与他们合作,或开发自己的数字产品来对抗这些新兴金融科技公司。 其中有花旗投资公司C2FO,BlueVine,FastPay以及摩根大通在Prosper,LevelUp和Gopago的投资。

现在,金融科技公司似乎在努力变得更像银行一些。

尽管一些金融科技公司对银行文化感到不屑,客户了解程序(KYC)也十分繁琐,获得银行牌照仍然不失为一条被许多很酷的金融科技公司创始人信任的发展之路。我们发现,从支付领域到市场贷款领域的多家新兴金融科技公司都在试图获得银行章程。

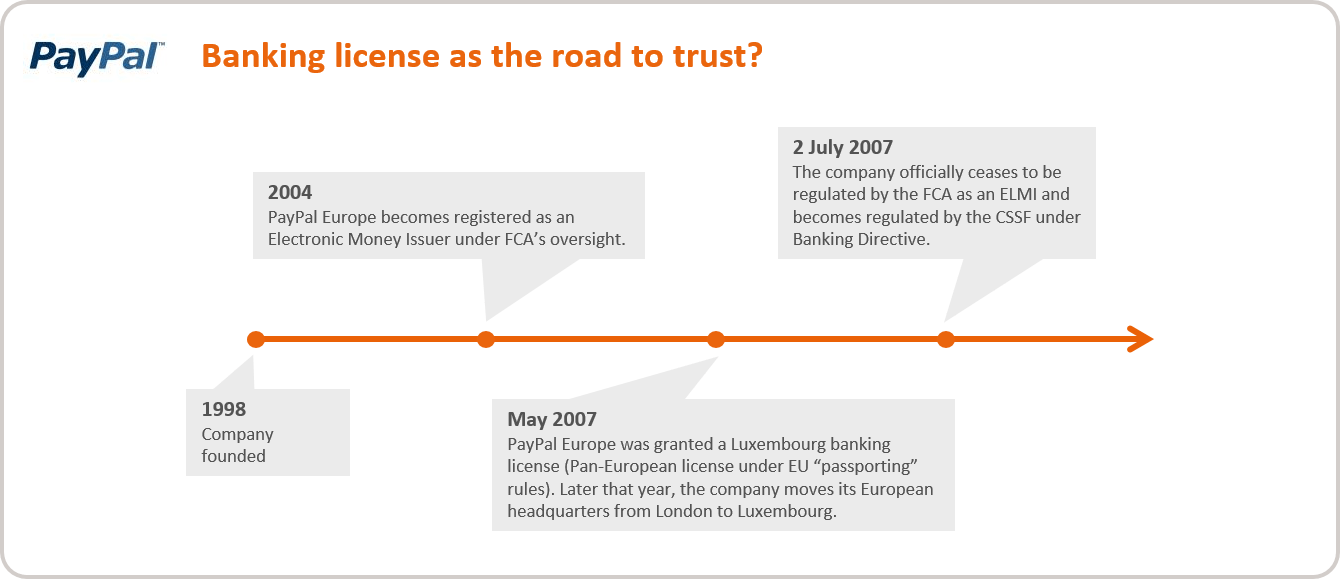

我们曾经见证PayPal采取这条路线。 它于2007年5月申请并随后获得了卢森堡银行牌照,由此在金融监管委员会监督的银行指令指导下开始了运营。 然而,金融科技公司银行业务类应用的份额量清楚地表明,全新的趋势已经出现了。

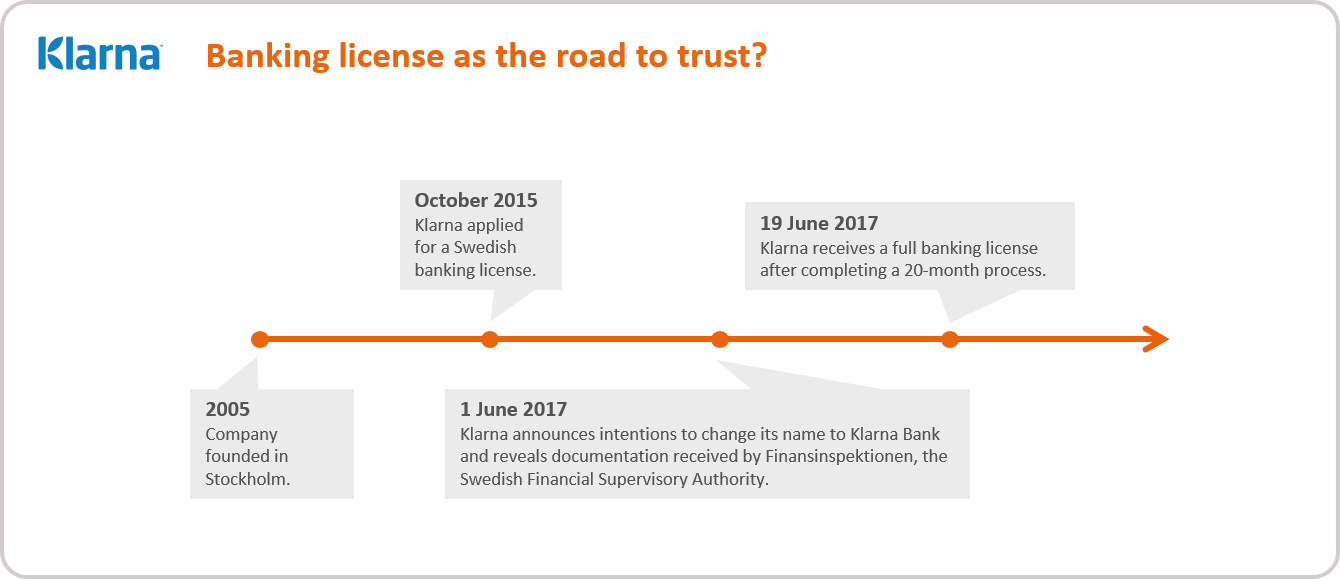

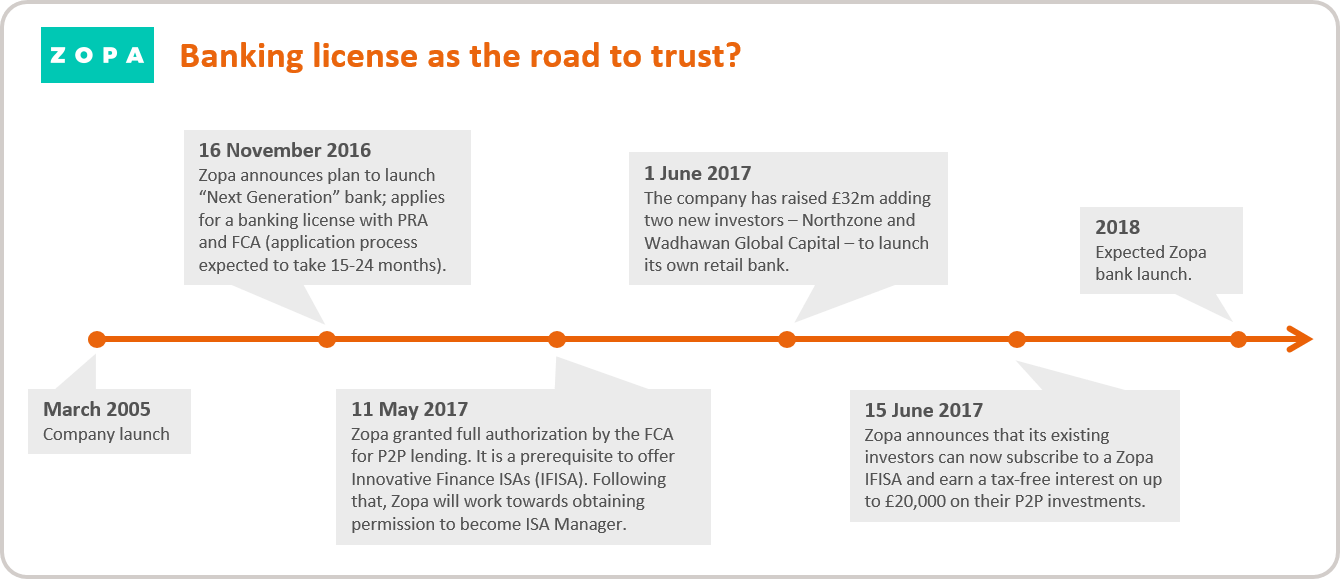

获得银行牌照基本上意味着金融科技公司无需再依赖与现有银行的合作伙伴关系。 然而,选择与现有银行合作可能是更小的金融科技公司更容易做出的选择。 如上表所示,银行章程申请可能是一个漫长而繁琐的过程——Klarna花了20个月才获得许可!

那么,金融科技公司选择持牌道路的原因可能有哪些呢?

尽管存在各种困难和麻烦,银行牌照仍可以为金融科技公司提供如下几个优势:

- 更广的业务规模和更大的客户群,特别是个人客户(存款!);

- 通过存款担保计划,获得个人存款人信任;

- 长期有效的资本基础;

- 在日益更加拥挤的金融科技创业领域获得竞争优势;

- 在整个行业生态系统验证其业务模式;

- 在欧盟单一市场上获利;

- 为PSD2创造新机会和公平的竞争环境。

银行牌照可以成为一系列全新的银行产品的开端,这些产品符合深受消费者喜爱的一站式格式数字化产品(即单一的综合数字银行应用程序)这一新兴趋势。 它也可能是营销或品牌感知方面的重大举措。 例如,金融科技公司可以发行品牌支付卡,通过这种方式允许基于互联网的公司进一步深入线下交易。

事实上,银行牌照可以被认为是金融科技终于获得更广泛的认可和合法性的证明。它将有助于消除金融科技面临的发展障碍和怀疑。 更重要的是,它在更广泛的金融环境中提升了金融科技公司的地位。数千家金融科技公司拥有不同的控制水平,一桩丑闻可能会对整个行业产生负面影响。 这在2016年的贷款俱乐部事件中显而易见。在这种情况下,银行牌照可能将成为一种区别因素。

“可能性艺术”之成本

由于更轻宽松(或缺乏)监管,金融科技公司一直被诟病与传统银行处于不同级别的竞争环境。随着越来越多的金融科技公司开始申请银行牌照并接受监管,这一状况将发生改变。这可被视为整个行业状况发生根本转变的信号。传统金融机构将无法再声称金融科技公司享有相对的监管优势。 这无疑给这些“现有玩家”们施加了压力,迫使他们在效率、成本、消费者导向和灵活性方面进行自我提升,特别是在面对所谓的千禧一代消费者时。

银行牌照也意味着额外的义务,如(增加的)资本要求,成本,程序和存款保险计划。 在面临与传统金融公司相同程度的监管的情况下,金融科技公司能否保持业务模式和竞争优势? 时间会说明一切。

关键问题仍然存在

这一商业模式将如何演变? 金融科技公司能在保持其成本优势的同时,保持“酷、小而敏捷”的吸引力吗? 他们会继续对现有银行的建立产生积极影响吗? 银行1.0能否修复其在消费者心中的消极形象和声誉? 银行1.0,银行 2.0和无银行执照的金融科技公司之间的差距是会扩大还是缩小?

从更广阔的角度来看,这种追逐银行许可证的趋势可能有助于创造一个更强大和安全的金融科技生态系统。

十年前谁会想到,2017年PayPal的市值将是德意志银行的两倍? 有一件事是肯定的:在未来十年的时间里,银行业的景观将会非常,非常,非常...不同。

非常感谢您的报名,请您扫描下方二维码进入沙龙分享群。

非常感谢您的报名,请您点击下方链接保存课件。

点击下载金融科技大讲堂课件本文系未央网专栏作者发表,属作者个人观点,不代表网站观点,未经许可严禁转载,违者必究!

本文为作者授权未央网发表,属作者个人观点,不代表网站观点,未经许可严禁转载,违者必究!

本文版权归原作者所有,如有侵权,请联系删除。

京公网安备 11010802035947号

京公网安备 11010802035947号